The Hundred-Year Bottleneck

Why Innovation Isn’t Making Us Richer

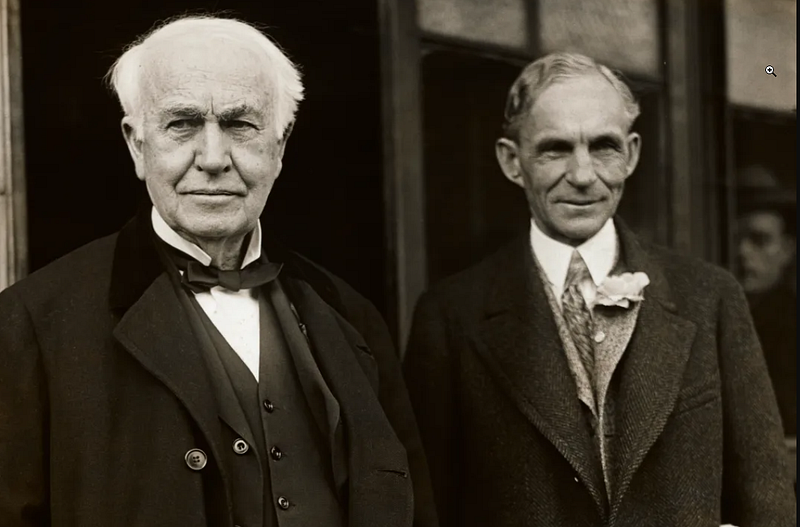

In 1921, the two most respected industrialists in America sat down to explain why the monetary system was strangling innovation.

Henry Ford had revolutionized manufacturing. Thomas Edison had electrified civilization. Between them, they had done more to raise human living standards than perhaps any two people in history. And they were really, really pissed about money.

“The function of money is to facilitate the exchange of goods and services,” Ford told the New York Tribune. “The banking system has turned it into a game of Monopoly. Instead of serving production, finance has become the master of production.” Not his exact words!

Edison was blunter: “People don’t understand this money question. If they did, the present system could not last twenty-four hours. It is based on nothing but a gigantic swindle.” His exact words!

These weren’t radicals or cranks (well, on some days they were). Still, these were the men who had built modern America. And they saw something that most economists still refuse to see: the monetary system doesn’t just measure productive activity. It shapes it, constrains it, and increasingly, suffocates it.

The Paradox of Our Time

We live in an age of miracles.

A device in your pocket contains more computing power than NASA used to reach the moon. You use it to argue with strangers and watch videos of cats. Medical imaging can detect cancers invisible to the human eye. Robotic systems can manufacture goods with precision measured in microns. Artificial intelligence is beginning to augment human cognition itself. We can literally edit the human genome.

Real wages for American workers have been essentially flat since 1971. A single income that could support a family of four in 1965 now barely covers rent. Your grandfather bought a house on a factory salary. You have a master’s degree and three roommates. Young people delay families, delay homeownership, delay children, delay life itself. Not because they lack skills or work ethic, but because the math doesn’t work, it hasn’t worked for fifty years.

We put a man on the moon in 1969 with slide rules and pocket protectors. Today, we have supercomputers in our pockets and can’t afford the houses our parents bought.

How is this possible? How can we have unprecedented technological capacity and stagnating prosperity simultaneously?

The conventional answers don’t satisfy. Globalization? Automation? Declining unions? Avocado toast? Each explains a piece, but none explains the timing. Something changed around 1971, and that something wasn’t robots. It wasn’t trade deals. It wasn’t your breakfast choices.

What changed was money.

The Essential Problem with Gold

If you’re reading this, you probably already know that fiat currency is problematic. Since Nixon closed the gold window in 1971, the dollar has lost over 85% of its purchasing power. Savings decay. Debt compounds. The disciplined are punished while the leveraged are rewarded.

The natural response is to look backward: return to the gold standard. Anchor money to something real. Restore the discipline that constrained governments for millennia.

I used to think this way. Then I studied what Ford and Edison actually proposed, and I realized the problem goes deeper.

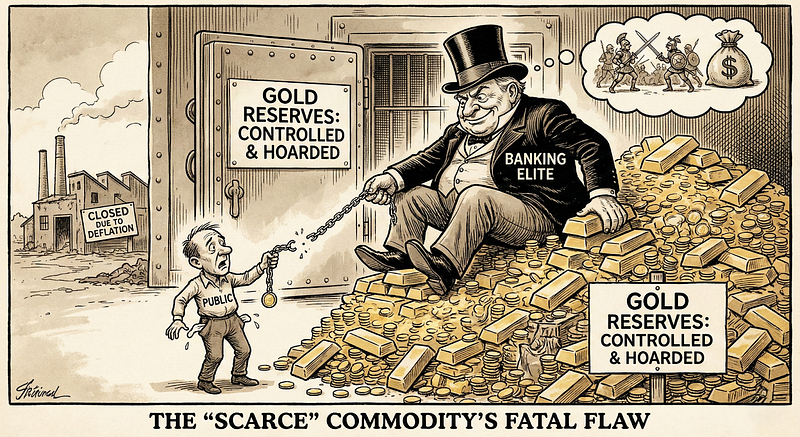

This isn’t theory. It’s history. The boom-bust cycles that plagued the nineteenth century weren’t caused by government intervention in a pure gold system. They were caused by the manipulation of a gold system by those who controlled the gold.

“The essential evil of gold in its relation to war is the fact that it can be controlled,” Ford declared. “Break the control, and you stop war.”

Gold wasn’t abandoned in 1971 because it was too restrictive. It was abandoned because it was too controllable by the wrong people. Foreign governments were redeeming their paper dollars for American gold at an alarming rate. France literally sent a warship to collect. They’d figured out the rules of the scam and started winning. So Nixon took his ball and went home. The discipline that gold imposed had become inconvenient for those in power, so they simply ended it.

Any system that can be ended by decree is vulnerable to being ended by decree. And it will be. The moment it becomes inconvenient for the people holding the decree pen.

Ford’s Alternative

Ford didn’t want to go back to gold. He wanted to go forward to something better. Money backed by energy, Thermodynamics is hard to cheat.

In 1921, he proposed to develop the Muscle Shoals dam complex on the Tennessee River using a new kind of money: currency issued directly against the productive capacity of the facility itself.

The dam would generate a predictable amount of electricity year after year. That electricity would power factories producing real goods. The output was physical, measurable, and governed by the laws of nature. Not the whims of bankers. Not the campaign contributions of politicians. Physics.

Ford proposed that the government issue currency against this productive capacity. No bonds. No interest payments. No bankers collecting tribute for the privilege of using the nation’s own credit.

“What I am proposing is that we substitute money based on the imperishable natural wealth of the nation for money based on a debt to private banks,” Ford explained. The currency would represent “a unit of power, a certain amount of energy exerted for one hour.”

Edison, the man who understood electricity better than anyone alive (with the possible exception of Tesla, who expressed similar sentiments ), [1] enthusiastically endorsed the plan.

The popular response was overwhelming. Ford received over one million letters of support. Farmers crushed by debt and deflation saw him as their champion. The South saw industrialization. Workers saw jobs.

For a moment, it seemed possible.

Then the bankers and politicians killed it. Because of course they did.

Why Every Reform Fails

The Ford proposal crashed on the same rocks that have wrecked every monetary reform for the past century.

Wall Street understood exactly what Ford was proposing. If the government could finance public works by issuing currency directly against productive assets, why would it ever need to borrow from banks? The entire edifice of public debt, the foundation of bank profits, would crumble. Can’t have that.

Agents of the monied class, the financial press attacked the plan as “unsound.” Editorials warned darkly of inflation (similar to the FUD spread about Bitcoin) [2]. Congressmen who depended on bank campaign contributions discovered urgent objections. Senators who couldn’t balance their own checkbooks suddenly became experts in monetary theory. Economists who’d spent their careers justifying the existing system found flaws that, coincidentally, protected the existing system.

Meanwhile, progressive reformers who agreed with Ford’s critique of Wall Street opposed his solution because it involved private operation of public resources. Ford found himself attacked from the right as a monetary radical and from the left as a robber baron.

Neither faction engaged seriously with the energy currency concept itself. The actual merits of anchoring money to productive capacity were never debated. That’s not what the debate was about. The debate was about power. It always is.

In 1924, Ford withdrew his offer. “I have tried to do something that would benefit the people,” he said, “and I have been blocked at every turn by the same forces that always block progress.”

This is the pattern that repeats for a hundred years. Same play, different actors.

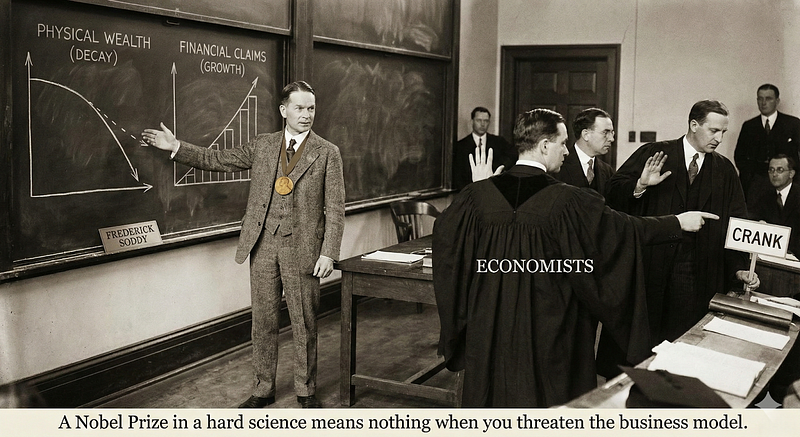

Frederick Soddy, a Nobel laureate in chemistry, spent the 1920s demonstrating that the financial system confused two incompatible categories: physical wealth (which decays according to thermodynamics) and financial claims (which grow according to compound interest). He proposed reforms. The economists dismissed him as a crank. A Nobel Prize in a hard science means nothing when you threaten the business model.

The Technocrats of the 1930s designed an elaborate system of “Energy Certificates” that would measure economic activity in physical units. Their diagnosis was brilliant; their cure was totalitarian. The movement collapsed.

Buckminster Fuller proposed a Global Energy Grid that would stabilize currencies through interconnected electrical systems. It required international cooperation that the Cold War made impossible.

Friedrich Hayek demonstrated that government monetary monopoly was the root problem and proposed competitive private currencies. His solution required governments to permit competition, good luck with that! Asking the house to approve a game where the house doesn’t always win. Like asking Congress to stop insider trading. Perl Clutching!

Every single attempt failed. Not because the diagnosis was wrong, but because every solution required permission from the people who benefit from the current system.

It’s a big club. It’s really not, but you ain’t in the 1%.

The Innovation Tax

Let me bring this back to innovation.

Productive activity, making things, building things, creating things that didn’t exist before, is the source of all genuine wealth. When Ford built a factory, he transformed raw materials and human effort into automobiles that made life better for millions of people. That’s wealth creation. He increased the wages of his workers so they could buy the things they were making. Real Innovation that did not go down well with the other robber barons of the time. Because the monetary system doesn’t reward wealth creation. It rewards wealth capture.

Under the current system, money is created primarily through debt. Banks create money out of thin air and charge interest. Governments borrow money into existence and service the debt through taxation and inflation. The entire apparatus is designed to siphon value from productive activity toward the investor class.

This creates a systematic bias against innovation.

Innovation requires long time horizons. You invest today, hoping to reap rewards in five, ten, or twenty years. But when money loses 3–7% of its purchasing power annually, those future rewards shrink before you receive them. The return on patience is negative. So patience disappears. Why build something real when you can flip something fake?

Innovation requires capital accumulation. You save from current production to fund future production. But when savings decay and debt is subsidized, accumulation is punished. The disciplined saver loses to the leveraged speculator. Every time. By design.

Innovation requires accurate price signals. You need to know what things actually cost to allocate resources efficiently. But when the unit of measurement keeps changing, when the ruler shrinks 3% every year, all your calculations are distorted. You’re trying to build a house with a tape measure that lies to you.

The monetary system isn’t neutral. It’s an invisible tax on creation and a subsidy to extraction. It doesn’t prevent innovation entirely, but it ensures that innovators capture only a fraction of the value they create. The rest is siphoned away by those who control the measuring stick. The design was not intended to punish the working class, but you can bet your buttons it was intended to benefit the wealthy.

This is why real wages have stagnated despite miraculous productivity gains. The gains are real. The distribution mechanism is rigged.

You work harder. You produce more. They take more. And then they lecture you about productivity.

The Structural Solution

For a century, reformers tried to fix the monetary system through political action. Lobby Congress. Elect better politicians. Appoint wiser central bankers. Educate the public.

None of it worked because the system protects itself. The people with the power to change the rules benefit from the existing rules. Asking them to reform is asking them to impoverish themselves. How do you think that vote goes?

Then, in 2008, two things happened: my bullshit meter broke, and someone stopped asking permission.

Bitcoin doesn’t petition governments to reform monetary policy. It doesn’t lobby central banks. It doesn’t require anyone’s permission. And I stopped watching the news.

Bitcoin simply offers an alternative: money that can’t be printed by decree, [3] can’t be controlled by banks, can’t be manipulated by anyone. Money that is anchored to physical reality through the thermodynamic cost of computation. Money that rewards saving rather than punishing it.

This is what Ford and Edison were reaching for in 1921. A currency backed by energy rather than debt. Thermodynamic Security: They couldn’t build it because the technology didn’t exist. The consensus problem that stymied every previous attempt required a solution that wouldn’t be discovered for another eighty years.

Today, the hundred-year problem has been solved. Not through politics. Through engineering Innovation.

A Note to Skeptics

I understand the skepticism. I shared it at first.

Bitcoin looks strange from within the traditional finance paradigm. It has no earnings, no yield, no underlying business. It doesn’t fit the mental models we’ve been trained to use. It sounds like something a guy with a podcast would try to sell you.

But here’s the thing about those mental models: they were built for a world where money was stable. Or at least where its instability was hidden well enough to ignore. Where you could pretend the ruler wasn’t shrinking. Where you could model the future without accounting for the fact that every dollar in your project is worth less than the dollar before it.

That world is ending. The instability is becoming impossible to hide. The Fed printed more money in 2020 than existed in 2000. Let that sink in. Everything that existed in the economy at the turn of the millennium, every factory, every business, every house, every car. They conjured that much purchasing power out of thin air in a single year. And then they acted surprised when prices went up. Shocking. Who could have predicted?

You can keep playing the game. Lots of smart people do. They arbitrage the chaos, front-run the Fed, trade the volatility. Some of them get rich. Most of them are just running faster to stay in place, skimming basis points while the foundation rots. They’ll tell you they’re sophisticated. They’re not sophisticated. They’re complicit. There’s a difference.

The question isn’t whether Bitcoin is a perfect monetary system. Nothing is perfect. The question is whether it’s better than a system designed to extract value from productive activity and transfer it to the investor class. Whether it’s better than a system that punishes savers, rewards debtors, and taxes innovation through perpetual currency debasement. Whether it’s better than a system where the rules change whenever the people who write the rules start losing.

That’s a low bar. Bitcoin clears it.

Ford and Edison saw the problem a hundred years ago. They proposed a solution that required permission from the people it threatened. The permission was denied.

Bitcoin requires no permission. It just requires adoption. One person at a time, one transaction at a time.

The door is open. You can walk through it or not. You can keep arguing about whether the door is real while the building burns. Your call.

But at least now you know it exists.

Brian Connelly is the author of “Before Satoshi: The Hundred-Year History of Bitcoin” and “How to Keep Your Bitcoin Alive and Well.” He spent thirty years as a systems architect and strategic consultant before turning to Bitcoin education.

[1]”Money does not represent such a value as men have placed upon it. All my money has been invested into experiments with which I have made new discoveries enabling mankind to have a little easier life.” Tesla believed in a “law of compensation” -the idea that true rewards should be proportional to the labor and energy sacrificed. This mirrors Ford’s argument that money should be a “unit of work” rather than a tool for interest-bearing debt.

[2] “Ponzi scheme.” “Tulip mania.” “Only used by criminals.” “It’s going to Zero” The slogans change. The playbook doesn’t. Bitcoin died at least 450 times

[3] Note and offer not a decree.